Are your savings sitting in an account earning next to nothing? You want your money to work harder for you, but maybe high-risk investments aren’t your style. You might have heard about “money market” options but feel lost in the jargon. If you’re asking, “what is a money market saving account?“, you’ve come to the right place. While often called that, the technically correct term is Money Market Account (MMA) or Money Market Deposit Account (MMDA). This guide will break down exactly what an MMA account is, how it works, its pros and cons, how it compares to other savings vehicles, and most importantly, if it’s the right choice for your money in 2025.

Table of Contents

Demystifying the Name: Money Market Account (MMA) vs. Money Market Saving Account

First things first, let’s clear up the naming. While many people search for “money market saving account,” the product offered by banks and credit unions is officially called a Money Market Account (MMA) or, more formally, a Money Market Deposit Account (MMDA).

Why the confusion? Because MMDAs blend features of both savings and checking accounts, acting as a type of high-powered savings vehicle. Throughout this article, we’ll primarily use the common term Money Market Account (MMA).

Crucial Distinction: It’s vital not to confuse a bank’s MMA/MMDA with a Money Market Mutual Fund (MMMF).

- MMAs/MMDAs: Offered by banks/credit unions, function like deposit accounts, are FDIC or NCUA insured (up to current limits). They are very safe places for cash.

- MMMFs: Are investment products offered by brokerage firms, invest in short-term debt, are NOT FDIC/NCUA insured, and carry a small risk of losing principal (though rare).

This article focuses exclusively on the bank/credit union Money Market Accounts (MMAs/MMDAs).

So, What Is a Money Market Account (MMA)? The Core Definition

At its heart, a Money Market Account (MMA) is a type of interest-bearing deposit account offered by banks and credit unions. Think of it as a hybrid account that combines some of the interest-earning potential you might associate with savings goals with some of the accessibility features you get from a checking account.

They are designed to offer savers a safe place to park their cash while potentially earning a higher interest rate than a traditional savings account, coupled with easier access to funds.

How Do Money Market Accounts Work? The Nuts and Bolts

MMAs operate similarly to other bank accounts but have some distinct characteristics:

Earning Interest: Variable Rates & APY

- MMAs pay interest on your balance. The key thing to know is that this interest rate is typically variable, meaning it can change over time based on prevailing market interest rates set by institutions like the Federal Reserve and the bank’s own policies.

- Rates are usually expressed as an Annual Percentage Yield (APY). APY reflects the total amount of interest you will earn in a year, including the effect of compounding (interest earning interest). This makes APY the best metric for comparing rates between different accounts.

- Often, MMAs may have tiered interest rates, meaning you might earn a higher APY if your balance exceeds certain thresholds (e.g., $10,000, $50,000).

Accessing Your Funds: Checks, Debit Cards, and Transfers

- One of the defining features of MMAs is their accessibility. Unlike some savings accounts or CDs, most MMAs allow you to access your money relatively easily.

- Common access methods include:

- Check Writing: Many MMAs come with check-writing privileges, though sometimes limited in number per month.

- Debit Card: Some MMAs offer an ATM/debit card for withdrawals and purchases.

- Electronic Transfers: You can typically transfer funds electronically between your MMA and other linked accounts (like your checking account).

- Branch Withdrawals: Access via tellers at physical bank locations (if available).

- Important Note on Limits: Historically, Regulation D limited certain types of withdrawals and transfers from savings and money market accounts to six per month. While the Federal Reserve removed this requirement in 2020, many banks still impose their own monthly transaction limits on MMAs. Exceeding these limits can result in fees or even account conversion/closure. Always check the specific bank’s policy.

Minimum Balances & Fees

- MMAs often require a higher minimum opening deposit compared to basic savings accounts (ranging from $0 at some online banks to $2,500, $10,000, or even more at others).

- Many also require you to maintain a minimum daily or average monthly balance to earn the stated APY or, more commonly, to avoid a monthly maintenance fee. Falling below this threshold can result in fees that quickly negate any interest earned.

Key Features & Benefits of Money Market Accounts

Why choose an MMA over other options? Here are the main advantages:

- Potentially Higher Interest Rates than Traditional Savings

- This is often the biggest draw. While not always guaranteed, MMAs typically offer APYs significantly better than standard brick-and-mortar savings accounts, allowing your cash reserves to grow faster.

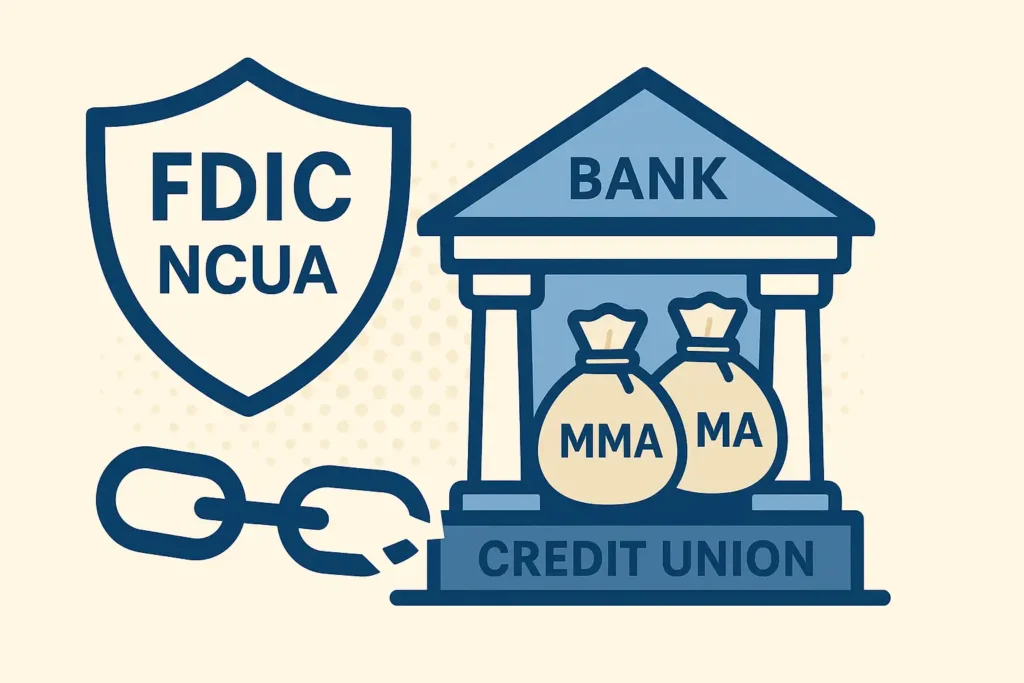

- Safety and Security (FDIC/NCUA Insurance)

- This is paramount. MMAs held at FDIC-insured banks or NCUA-insured credit unions are protected against bank failure. Your deposits are insured up to $250,000 per depositor, per insured institution, for each account ownership category (as of April 2025). This makes them a very safe place for your emergency fund or short-term savings goals. Verify your bank’s insurance status via the FDIC’s BankFind tool.

- Enhanced Liquidity and Access

- Compared to less accessible options like Certificates of Deposit (CDs), MMAs offer good liquidity. The ability to write checks, use a debit card, or make electronic transfers provides flexibility when you need access to your funds without penalty.

- Check-Writing & Debit Card Privileges

- These features bridge the gap between savings and checking, making MMAs convenient for occasional large payments or ATM access directly from your interest-earning account.

Potential Drawbacks & Considerations for MMDAs

Before opening an MMA, be aware of the potential downsides:

- Variable Interest Rates Mean Uncertainty

- Unlike CDs with fixed rates, the APY on your MMA can decrease if market rates fall. You don’t have the rate certainty of a CD.

- Higher Minimum Balance Requirements

- The need to maintain a substantial minimum balance to avoid fees can be a barrier for some savers. If you can’t consistently meet the minimum, fees could wipe out your earnings.

- Transaction Limits Can Be Restrictive

- Even though Reg D limits are gone at the federal level, bank-imposed limits on certain withdrawals (often 6 per month for checks, debit card uses, certain transfers) can be inconvenient if you need frequent access beyond basic ATM withdrawals or teller transactions.

- Fees Can Add Up

- Watch out for monthly maintenance fees (if minimums aren’t met), excessive transaction fees, ATM fees (if using out-of-network machines), and potentially others. Read the fee schedule carefully.

- Rates May Lag Behind High-Yield Savings Accounts (HYSAs)

- While often better than traditional savings, MMA rates might sometimes be slightly lower than the top online-only High-Yield Savings Accounts, which often have fewer overhead costs.

Money Market Account vs. Traditional Savings Account: What’s the Difference?

Here’s a quick comparison:

| Feature | Money Market Account (MMA) | Traditional Savings Account |

|---|---|---|

| Interest Rate | Potentially Higher, Variable | Typically Lower, Variable |

| Access | Checks, Debit Card, Transfers, ATM, Branch | Transfers, ATM, Branch (No Checks/Debit) |

| Min. Balance | Often Higher Requirement to Avoid Fees | Usually Lower or No Requirement |

| Fees | Possible Monthly Fee if Below Minimum | Generally Fewer Fees |

| Best For | Earning more interest with easy access | Basic savings, lower balance needs |

Money Market Account vs. High-Yield Savings Account (HYSA): A Closer Look

HYSAs, often found at online banks, are another popular option. How do they stack up against MMAs?

- Rate Potential: Often very competitive. Sometimes top HYSAs edge out MMAs slightly, sometimes it’s the reverse. Both typically offer much better rates than traditional savings.

- Access Features: This is the main difference. HYSAs generally do not offer check-writing or debit card access. Access is primarily through electronic transfers to/from linked accounts or sometimes ATM cards (less common). MMAs usually offer more direct access methods.

- Minimum Balances/Fees: Both can have minimums, but many online HYSAs have low or no minimum balance requirements and fewer fees compared to some traditional bank MMAs.

- Which is Better? If maximum APY and simple online transfers are your priority, an HYSA might win. If you value the convenience of check-writing or debit card access directly from your interest-bearing account, an MMA could be preferable, even if the rate is fractionally lower.

Money Market Account vs. Certificate of Deposit (CD): Understanding Liquidity Trade-offs

CDs are another savings tool, but they function differently:

- Rate Structure: CDs typically offer a fixed interest rate for a specific term (e.g., 6 months, 1 year, 5 years). This rate is locked in, unlike the variable rate of an MMA. CD rates may be higher than MMA rates, especially for longer terms, but not always.

- Access/Liquidity: This is the key trade-off. With a CD, your money is locked up for the entire term. Withdrawing funds before the maturity date usually incurs a significant early withdrawal penalty, potentially costing you some or all of the interest earned, or even part of the principal. MMAs offer much greater flexibility to access funds without penalty (provided you stay within transaction limits).

- When to Choose Which: CDs are suitable for funds you know you won’t need for a specific period and when you want rate certainty. MMAs are better for funds you might need access to sooner or for building an emergency fund where liquidity is key.

Are Money Market Accounts Safe? Understanding FDIC/NCUA Insurance

Yes, Money Market Accounts (MMDAs) held at federally insured institutions are very safe, provided your balance stays within the insurance limits.

- How Coverage Works:

- The Federal Deposit Insurance Corporation (FDIC) insures deposits at member banks.

- The National Credit Union Administration (NCUA) insures deposits at member credit unions (via the National Credit Union Share Insurance Fund – NCUSIF).

- Coverage is $250,000 per depositor, per insured institution, per account ownership category. (e.g., single accounts, joint accounts, certain retirement accounts have separate coverage).

- This means if the bank fails, the government insurance fund will reimburse your deposits up to the limit.

- The Critical Distinction (Again!): Remember, this safety net applies only to MMDAs at banks/credit unions. It does NOT apply to Money Market Mutual Funds (MMMFs) from investment firms. While MMMFs are generally considered low-risk investments, they can lose value and are not government-insured. Understanding this difference is crucial for managing risk. For more on investment product safety, consult resources like Investor.gov.

Who Should Consider Opening a Money Market Account?

An MMA can be a smart choice for several types of savers:

- Building an Emergency Fund: The combination of safety (FDIC/NCUA insurance), better-than-basic interest rates, and relatively easy access makes MMAs ideal for holding 3-6 months’ worth of living expenses.

- Saving for Short-to-Medium Term Goals: If you’re saving for a down payment on a house, a new car, or a big vacation within the next few years, an MMA keeps your funds safe while earning some interest.

- Parking Large Sums Temporarily: If you’ve received a windfall (like an inheritance or bonus) and need time to decide on long-term investments, an MMA offers a safe, liquid place to park the cash while earning interest.

- Those Wanting Higher Rates Than Basic Savings with Check/Debit Access: If the convenience features are important to you, an MMA might be worth it even if an online HYSA offers a slightly higher APY.

How to Choose the Best Money Market Account for You

Ready to shop around? Here’s what to compare:

- Compare APYs: Look for the highest Annual Percentage Yield, but don’t stop there. Check if it’s an introductory rate that might drop later. Understand any balance tiers.

- Check Minimum Deposit & Balance Requirements: Ensure you can meet the initial deposit and ongoing balance requirements to earn the advertised APY and avoid fees.

- Understand ALL the Fees: Look beyond the monthly maintenance fee. Are there fees for excessive transactions, out-of-network ATMs, check printing, etc.? Read the fine print.

- Evaluate Access Options: How easily can you get your money? Consider online/mobile banking quality, ATM network size and fees, check-writing availability, and branch access if important to you.

- Verify FDIC/NCUA Insurance: Only deposit funds in insured institutions. Use the FDIC/NCUA website tools to confirm.

Conclusion: Is a Money Market Account Right for Your Savings Strategy?

So, what is a money market saving account (or more accurately, an MMA/MMDA)? It’s a secure, interest-bearing deposit account offering a potential rate boost over traditional savings, coupled with convenient access features like check-writing and debit cards. While potentially requiring higher minimum balances and having variable rates, its FDIC/NCUA insurance makes it a safe harbor for emergency funds and short-term goals.

By understanding how MMAs work and comparing them to other options like HYSAs and CDs, you can determine if they fit strategically within your overall financial plan. They offer a compelling blend of safety, yield, and accessibility for many savers in 2025.

Frequently Asked Questions (FAQ) about Money Market Accounts

Can I lose money in a bank money market account (MMA/MMDA)?

Assuming the bank is FDIC or NCUA insured, and your deposit is within the $250,000 limit per depositor/institution/ownership category, you cannot lose your principal due to bank failure. The value of your deposit doesn’t fluctuate with the market like an investment. However, fees could erode your balance if you don’t meet minimums, and inflation can erode the purchasing power of your savings over time, as MMA rates typically don’t outpace high inflation. You can lose money in non-insured Money Market Mutual Funds (MMMFs).

What’s the main advantage of a money market account over regular savings?

Usually, it’s twofold: Potentially higher interest rates (APY) allowing your money to grow faster, and enhanced access features, particularly the ability to write checks or use a debit card directly from the account, which most standard savings accounts lack.

Are there still limits on how many withdrawals I can make from an MMA?

While the federal Regulation D limit of six certain types of transactions per month was removed, many banks still impose their own monthly limits (often six) on non-teller/ATM withdrawals like checks, debit card purchases, and certain electronic transfers. Exceeding these can lead to fees. Always check your specific bank’s account agreement.

Do money market accounts keep up with inflation?

Generally, no. MMAs are designed for safety and liquidity, not high growth. While they offer better rates than traditional savings, their returns typically lag behind the rate of inflation, meaning the purchasing power of your money may decrease over time. For inflation-beating growth, you generally need to consider investments with higher potential returns (and higher risk).

Call to Action:

Does a Money Market Account sound like a good fit for your savings goals? Have you had positive or negative experiences with MMAs? Share your thoughts or questions in the comments below! If this guide helped clarify what a money market account is, please consider sharing it with others who might benefit. Ready to explore options? Start comparing MMA offers from reputable banks and credit unions today.