Table of Contents

Savings Accounts Explained: Your Ultimate Guide to Choosing and Growing Your Money

Is your hard-earned cash just sitting in your checking account, maybe earning next to nothing? Or perhaps tucked away somewhere “safe” at home? While keeping some cash accessible is smart, letting significant amounts idle means you could be missing out on crucial growth and security. That’s where savings accounts come in. They might seem basic, but understanding them fully is a cornerstone of smart money management.

Confused about APYs, different account types, or how to pick the right one? You’re not alone. This guide cuts through the jargon. We’ll demystify savings accounts, explore how they work (hello, compound interest!), compare the different options available (from traditional banks to high-yield online accounts), and give you a clear roadmap to choose the perfect fit for your financial goals. Let’s turn that idle cash into a powerful tool for your future.

Decoding Savings Accounts: More Than Just a Place to Stash Cash

Before diving deep, let’s establish a clear understanding of what a savings account is and why it’s so fundamental.

Simple Definition: A Safe Haven for Your Money

At its core, a savings account is a deposit account held at a bank or credit union that allows you to store money you don’t need for immediate daily expenses. Its primary purposes are:

- Safety: Keeping your money secure, protected from loss or theft.

- Growth: Earning interest on your deposited funds, helping your money grow over time (albeit often modestly).

- Separation: Keeping savings separate from your everyday spending money (in your checking account) to reduce the temptation to spend it.

Think of it as a dedicated parking spot for your future goals, shielded from the hustle and bustle of daily transactions.

Savings vs. Checking Accounts: Key Differences Clarified

People often confuse savings and checking accounts, but they serve distinct purposes:

| Feature | Checking Account | Savings Account |

|---|---|---|

| Primary Use | Daily transactions (spending, bills) | Storing money, saving for goals |

| Access | Frequent (Debit card, checks, ATM) | Less frequent (Transfers, limited withdrawals) |

| Interest | Typically none or very low | Earns interest (APY varies) |

| Withdrawals | Unlimited (usually) | Often limited (e.g., 6 per month by Reg D*) |

| Goal | Convenience | Safety, Growth, Goal Achievement |

*Note: Regulation D limitations were removed by the Federal Reserve, but many banks still maintain withdrawal limits on savings accounts as a policy. Always check the specific account terms.

Using each account for its intended purpose is key to effective money management.

Why Do You Need a Savings Account? (Core Benefits)

- Security: Federally insured accounts protect your money up to legal limits.

- Earn Interest: Your money works for you, generating passive income.

- Emergency Fund: The ideal place to build a cushion for unexpected expenses (job loss, medical bills).

- Goal Achievement: Helps you systematically save for specific targets (down payment, vacation, new car).

- Financial Discipline: Separating savings discourages impulsive spending.

The Mechanics: Making Your Money Work for You

Understanding how savings accounts operate helps you appreciate their value and choose wisely.

Interest Rates & APY Explained (The Growth Engine)

Banks pay you interest because they use your deposited funds for lending and other activities.

- Interest Rate: The basic percentage the bank pays on your deposit.

- APY (Annual Percentage Yield): This is the real rate of return, reflecting the interest rate and the effect of compounding within a year. Always compare APYs when choosing an account.

Crucial Note (April 2025): Interest rates and APYs are not static. They fluctuate based on economic conditions and Federal Reserve policies. Rates that are competitive today might not be tomorrow. Regularly review your account’s APY and compare it to current market offerings. What constitutes a “high-yield” APY changes over time.

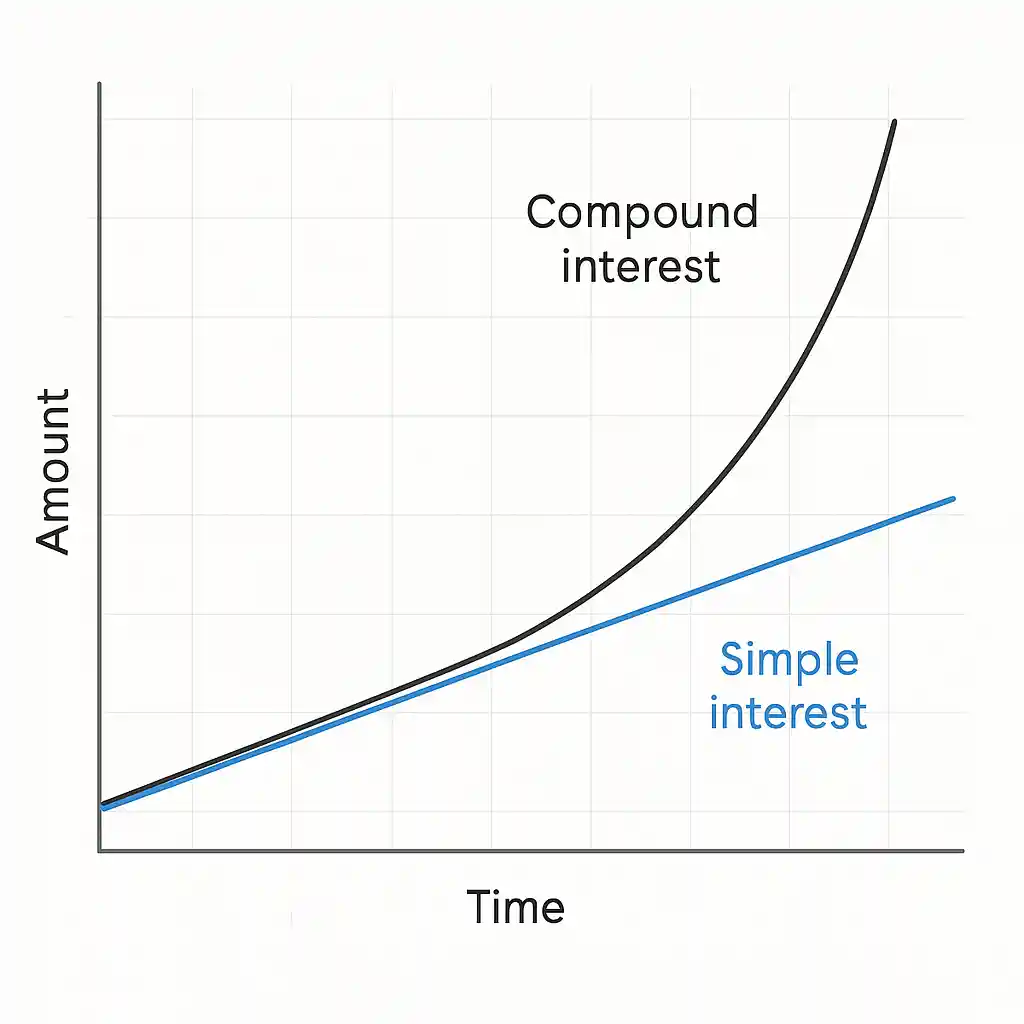

The Magic of Compound Interest (Why Starting Early Matters)

Compound interest is essentially earning interest on your interest. It creates a snowball effect, making your savings grow exponentially faster over time.

- Example: You deposit $1,000 into an account with a 4% APY.

- Year 1: You earn $40 in interest (Total: $1,040).

- Year 2: You earn 4% on $1,040 = $41.60 (Total: $1,081.60).

- Year 3: You earn 4% on $1,081.60 = $43.26 (Total: $1,124.86).

The longer your money stays deposited and compounds, the more significant the growth becomes. This highlights the power of starting to save early, even with small amounts.

Safety First: Understanding FDIC and NCUA Insurance

One of the biggest advantages of traditional bank and credit union savings accounts in the US is federal insurance.

- FDIC (Federal Deposit Insurance Corporation): Insures deposits at member banks, typically up to $250,000 per depositor, per insured bank, for each account ownership category.

- NCUA (National Credit Union Administration): Provides equivalent insurance (Share Insurance Fund) for deposits at member credit unions.

This insurance means that even if the bank fails, your insured deposits are protected by the U.S. government. Always verify that your chosen institution is FDIC or NCUA insured. You can typically find this information on the institution’s website or by using the FDIC’s BankFind tool (https://www.fdic.gov/resources/bank-find/) or the NCUA’s Credit Union Locator (https://mapping.ncua.gov/).

Not All Savings Accounts Are Created Equal: Exploring Your Options

The term “savings account” covers several variations. Knowing the differences helps you match an account to your needs.

Traditional Savings Accounts (Brick-and-Mortar Banks)

- What they are: Standard accounts offered by large national banks or smaller community banks with physical branches.

- Pros: Convenient branch access, potential relationship benefits, often easy to link with existing checking.

- Cons: Typically offer very low APYs compared to online options, may have higher fees or minimum balance requirements.

- Best for: Those who prioritize in-person service and convenience over maximizing interest earnings.

High-Yield Savings Accounts (Often Online)

- What they are: Accounts designed to offer significantly higher APYs than traditional savings accounts. Many are offered by online-only banks or online divisions of larger banks.

- Pros: Much higher interest rates (APYs), often lower or no monthly fees, low or no minimum balance requirements, strong online/mobile platforms.

- Cons: Limited or no branch access, cash deposits can be tricky (though often possible via ATM networks or transfers).

- Best for: Savers focused on maximizing growth and comfortable with digital banking. This is where you’ll typically find the most competitive rates.

Online Savings Accounts (Pros & Cons)

While many high-yield accounts are online, this category broadly refers to accounts primarily managed digitally.

- Pros: Higher APYs, lower fees, 24/7 access via web/app, often innovative features.

- Cons: No physical branches for troubleshooting, depositing cash can require extra steps, less personal relationship.

Money Market Accounts (MMAs)

- What they are: A hybrid between savings and checking accounts. They are insured deposit accounts.

- Features: Often offer tiered interest rates (higher balances may earn more), may come with check-writing privileges or a debit card (though transactions might still be limited).

- Comparison: APYs can sometimes be competitive with high-yield savings, but not always. They may have higher minimum balance requirements. MMAs are different from Money Market Funds, which are investment products and not FDIC/NCUA insured.

- Best for: Savers who want potentially higher rates than traditional savings and need limited check-writing or debit card access from their savings vehicle.

Specialty Savings Accounts (Kids, Goals, etc.)

- Kids’ Savings Accounts: Designed to teach children about saving, often with low minimums, no fees, and sometimes educational tools. May require an adult co-owner.

- Goal-Specific Savings: Some banks allow you to create “sub-accounts” or “buckets” within your main savings account to track progress towards different goals (e.g., “Vacation Fund,” “New Car Fund”).

Your Roadmap: How to Select the Right Savings Account

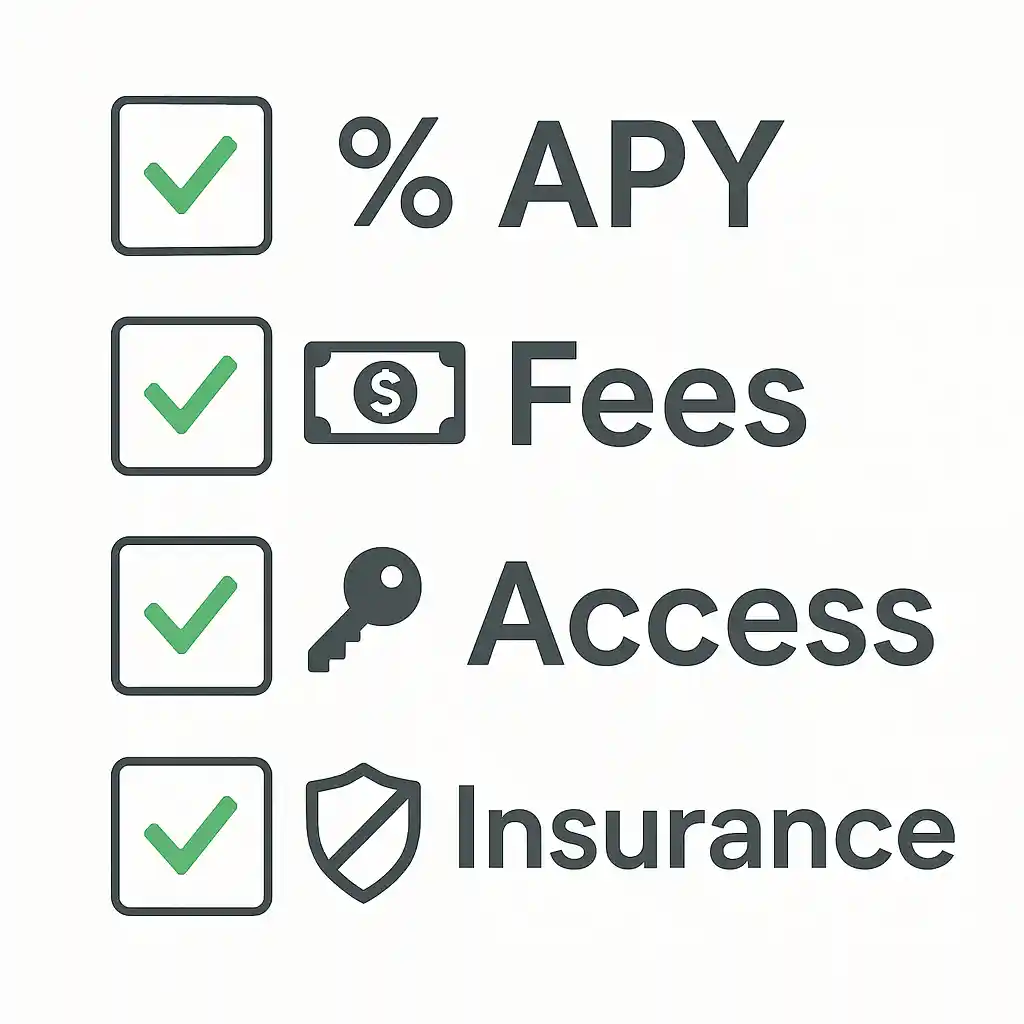

Choosing isn’t just about the highest number. Consider these factors holistically:

Factor 1: Interest Rate (APY) – Hunting for Yields

- This is often the biggest differentiator, especially with high-yield accounts.

- Action: Compare current APYs across different banks and credit unions (online banks often lead). Remember rates change – what’s highest today might not be next month. Use reputable financial news sites or comparison tools (be wary of sponsored results).

Factor 2: Fees (Monthly Maintenance, Overdraft, etc.) – The Hidden Costs

- High fees can quickly negate the interest earned. Look out for:

- Monthly maintenance fees (often waived if you meet minimum balance or direct deposit requirements).

- Excessive transaction fees (if you exceed withdrawal limits).

- Overdraft/Insufficient funds fees (less common for savings, but check linked accounts).

- Wire transfer fees, statement fees, etc.

- Action: Read the account’s fee schedule carefully. Aim for accounts with no monthly fees or fees that are easily avoidable for you.

Factor 3: Minimum Balance Requirements

- Some accounts require a minimum deposit to open or a minimum ongoing balance to avoid fees or earn the stated APY.

- Action: Ensure you can comfortably meet any minimums. Many excellent high-yield online savings accounts have no minimum balance requirements.

Factor 4: Access & Convenience (Online vs. Branch, Transfers)

- How easily do you need to access your money?

- Online/Mobile: How robust is the app/website? Easy transfers? Mobile check deposit?

- ATM Access: Is there a large, fee-free ATM network if you need occasional cash?

- Branch Access: How important is walking into a physical branch for you?

- Transfer Speed: How quickly can you move money between your savings and checking account (ACH transfers typically take 1-3 business days)?

- Action: Match the account’s access methods to your lifestyle and comfort level.

Factor 5: FDIC/NCUA Insurance (Non-Negotiable)

- As mentioned, ensure the institution is federally insured. This protects your principal.

- Action: Verify FDIC or NCUA membership. If you have very large deposits exceeding the $250,000 limit, research strategies for maximizing coverage across different banks or ownership categories.

Factor 6: Account Features & Tools

- Does the account offer helpful extras?

- Goal-setting tools or sub-accounts.

- Automatic savings plans (scheduling recurring transfers).

- Mobile check deposit.

- Integration with budgeting apps.

- Action: Consider which features would genuinely help you manage your savings more effectively.

Taking Action: Opening and Using Your Account Effectively

Once you’ve chosen an account, here’s how to get started and make the most of it.

The Opening Process (Online vs. In-Person)

- Online: Usually straightforward. You’ll typically need:

- Personal information (Name, address, DOB, Social Security Number/Tax ID).

- Government-issued ID (driver’s license, passport).

- Funding information (routing/account number for an existing bank account to make the initial deposit).

- The process often takes just a few minutes.

- In-Person: Visit a branch with the required documents. A banker will guide you through the application.

Tips for Maximizing Your Savings (Automation, Budgeting)

- Pay Yourself First: Treat saving like a bill. Set up automatic transfers from your checking to your savings account each payday or month. Even small, consistent amounts add up.

- Automate: This is the single most effective way to build savings consistently. Set it and forget it!

- Budget: Know where your money is going so you can identify areas to cut back and allocate more to savings.

- Save Windfalls: Deposit unexpected income (bonuses, tax refunds, gifts) directly into savings.

- Review Regularly: Periodically check your progress and the account’s APY. If rates have dropped significantly, consider switching to a more competitive account.

Common Mistakes to Avoid with Savings Accounts

- Choosing based only on convenience: Don’t sacrifice significant interest earnings for a nearby branch you rarely use.

- Ignoring Fees: Letting fees eat away at your interest.

- Dipping In Too Often: Treating it like a secondary checking account defeats its purpose (especially for emergency funds).

- Not Starting: Procrastinating because you think you don’t have “enough” to save. Start small!

- Forgetting About Inflation: Understand that low-interest savings accounts may not keep pace with inflation over the long term. They are for safety and short-to-medium-term goals, not long-term wealth growth (which typically requires investing).

Beyond the Basics: Integrating Savings Accounts into Your Financial Plan

Savings accounts aren’t just standalone products; they’re vital components of a healthy financial picture.

Building Your Emergency Fund: The Foundation

- This is arguably the most important use for a savings account, particularly a high-yield one.

- Goal: Aim for 3-6 months’ worth of essential living expenses.

- Location: Keep it liquid and safe in an FDIC/NCUA insured savings account, separate from your checking and investments. This fund protects you from debt when unexpected events occur.

Saving for Short-to-Medium-Term Goals

- Savings accounts are ideal for goals within the next ~5 years:

- Down payment on a house or car

- Upcoming vacation

- Wedding expenses

- Home repairs

- Property taxes

- The safety of principal is paramount for these goals, making insured savings accounts a better choice than potentially volatile investments.

How Many Savings Accounts Should You Have? (The Bucketing Strategy)

- There’s no single right answer, but many find having multiple savings accounts helpful.

- Strategy: Open separate accounts (or use sub-accounts/digital envelopes if offered) for different major goals (e.g., “Emergency Fund,” “House Down Payment,” “Travel Fund”).

- Benefits: Provides clarity on progress towards each goal, reduces the temptation to “borrow” from one goal for another. High-yield online banks often make opening multiple accounts easy and fee-free.

Quick Answers: Frequently Asked Questions About Savings Accounts

Let’s tackle some common queries:

- How much interest do savings accounts pay right now (April 2025)? Interest rates vary widely. Traditional banks might offer near 0%, while competitive high-yield online savings accounts could offer significantly more (e.g., potentially in the 4-5%+ APY range, but this changes constantly based on market conditions). Always check current rates directly with banks or reputable comparison sites.

- Are savings accounts completely safe? Can I lose money? If held at an FDIC or NCUA insured institution, your deposits are protected up to $250,000 per depositor, per bank, per ownership category, even if the bank fails. You won’t lose your principal within these limits. The main “risk” is that low interest rates may not keep pace with inflation, meaning your purchasing power could decrease over time.

- What’s the minimum amount needed to open a savings account? This varies. Many online high-yield savings accounts have no minimum opening deposit or ongoing balance requirement. Some traditional banks might require $25, $100, or more.

- Can I withdraw money from my savings account anytime? Yes, generally. However, access methods differ (transfers, ATM, branch). Also, while Regulation D limits are technically gone, many banks still enforce a limit of around 6 certain types of withdrawals/transfers per month to encourage saving. Check your account agreement.

- Should I choose an online bank or a traditional bank for my savings? It depends on your priorities. If maximizing interest (APY) and low fees are paramount, and you’re comfortable with digital banking, an online high-yield savings account is often the best choice. If you value in-person service and branch access above all else, a traditional bank might be preferred but expect much lower returns.

Start Saving Smarter Today

Savings accounts are fundamental tools for financial health. They provide a secure place for your emergency fund, help you reach specific goals, and allow your money to grow safely through the power of compound interest.

Choosing the right account involves looking beyond just the name on the building (or website). By comparing APYs (remembering they fluctuate!), understanding fees, checking accessibility, and ensuring FDIC/NCUA insurance, you can find an account that truly works for you. Don’t let analysis paralysis stop you – even starting with a small, automated deposit into a basic, insured savings account is a powerful first step.

Call to Action:

Ready to put your money to work? Take 15 minutes this week to compare high-yield savings accounts from reputable online banks and credit unions. Check their current APYs and fee structures. Even better, set up a small automatic transfer today!

What’s your biggest question about savings accounts, or what’s your favorite savings strategy? Share your thoughts in the comments below – let’s learn from each other! If this guide was helpful, please share it with friends or family who might benefit.